In today's hyperconnected financial ecosystem, the right set of fintech APIs can mean the difference between market leadership and obsolescence. As we navigate 2025, financial technology APIs have reached unprecedented sophistication, serving as the critical connective tissue binding innovative services together in the world of digital banking and financial services.

Table of Contents

The global API management market is experiencing significant growth, projected to reach around $43.8 billion by 2032, with a compound annual growth rate (CAGR) of approximately 34.7% from 2024 to 2032.

Having advised Fortune 500 companies on their digital transformation strategies for over two decades, I've witnessed firsthand how finance software APIs have evolved from simple data connectors to sophisticated engines driving entirely new business models. According to recent data from Gartner, organizations that strategically implement fintech API platforms experience 35% faster time-to-market and 42% reduction in development costs compared to their competitors.

This comprehensive guide cuts through the noise to deliver actionable insights on the most powerful top fintech APIs 2025 available today. Whether you're looking to revolutionize payment processing, harness the power of open banking, implement cutting-edge blockchain solutions, or enhance your wealth management offerings, this analysis will help you make informed decisions that drive your organization forward.

What Are Fintech APIs?

Financial technology APIs (Application Programming Interfaces) are specialized software intermediaries that allow different financial applications to communicate with each other. Unlike general-purpose APIs, finance software APIs are specifically designed to handle sensitive financial data, maintain regulatory compliance, and facilitate secure transactions across banking, payments, lending, and other financial domains.

The technical architecture of modern fintech APIs has evolved significantly since 2020. While RESTful APIs remain common, we're seeing increased adoption of GraphQL for its flexibility and efficiency in data retrieval. According to a 2024 study by API Evolution Research, GraphQL adoption in financial services has grown by 78% since 2022, primarily due to its ability to minimize network overhead and precisely deliver the requested data.

Architecture Type | Adoption Rate | Key Advantages | Best For |

|---|---|---|---|

RESTful APIs | 68% | Simplicity, caching, statelessness | General-purpose integration |

GraphQL | 27% | Precise data retrieval, reduced overhead | Data-intensive applications |

WebSockets | 18% | Real-time data streaming, persistent connection | Trading, live monitoring |

Webhooks | 62% | Event-driven architecture, push notifications | Transaction alerts, updates |

The most sophisticated fintech API platforms now incorporate:

Real-time streaming capabilities via WebSockets

Real-time streaming capabilities via WebSockets- Advanced authentication through OAuth 2.0 and Two-Factor Authentication (2FA)

- Robust data encryption both in transit and at rest

- Comprehensive audit logging for regulatory compliance

- Webhooks for event-driven architecture

- Sandboxed testing environments for fintech API integration

Why Fintech APIs Are Essential for Modern Finance Software

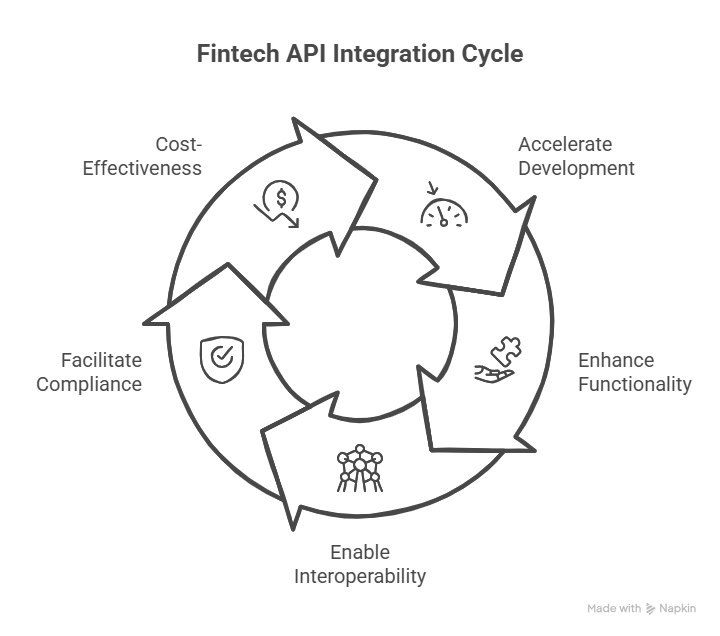

The strategic importance of finance software APIs cannot be overstated. According to McKinsey's 2024 Banking Technology Report, financial institutions leveraging third-party APIs reduced their product development cycles by an average of 68% while simultaneously expanding their service offerings by 47%.

Accelerating Development and Reducing Time-to-Market

Building financial functionality from scratch is prohibitively time-consuming and resource-intensive. By implementing proven fintech API solutions, development teams can focus on creating unique value propositions rather than reinventing fundamental capabilities.

Enhancing Functionality Without Building From Scratch

Modern financial technology APIs offer sophisticated capabilities that would be impractical to develop internally. From advanced fraud detection algorithms using machine learning to complex trading mechanisms, these APIs encapsulate years of specialized development and expertise that would otherwise require massive investment and specialized talent.

Enabling Interoperability Between Financial Systems

The fragmented nature of financial infrastructure has historically created silos that hamper innovation. Banking APIs bridge these gaps, allowing seamless integration between legacy systems and cutting-edge applications through microservices and API gateways. The International Data Corporation (IDC) estimates that improved interoperability through APIs generated $87 billion in value for the financial services industry in 2024 alone.

Facilitating Compliance With Financial Regulations

Financial services remain one of the most heavily regulated industries globally. Modern fintech APIs incorporate regulatory compliance as a core feature, automatically handling complex requirements like anti-money laundering (AML) checks, know-your-customer (KYC) procedures, and transaction monitoring. This dramatically reduces the compliance burden while ensuring consistent adherence to evolving regulations.

Cost-Effectiveness of API Integration vs. Custom Development

The economic case for fintech API adoption is compelling. A 2024 analysis by Financial Technology Partners found that financial institutions saved an average of $3.2 million per major project by leveraging specialized APIs rather than developing equivalent functionality in-house. This cost advantage becomes even more significant when factoring in maintenance, security updates, and ongoing compliance requirements for finance software.

Key Categories of Fintech APIs in 2025

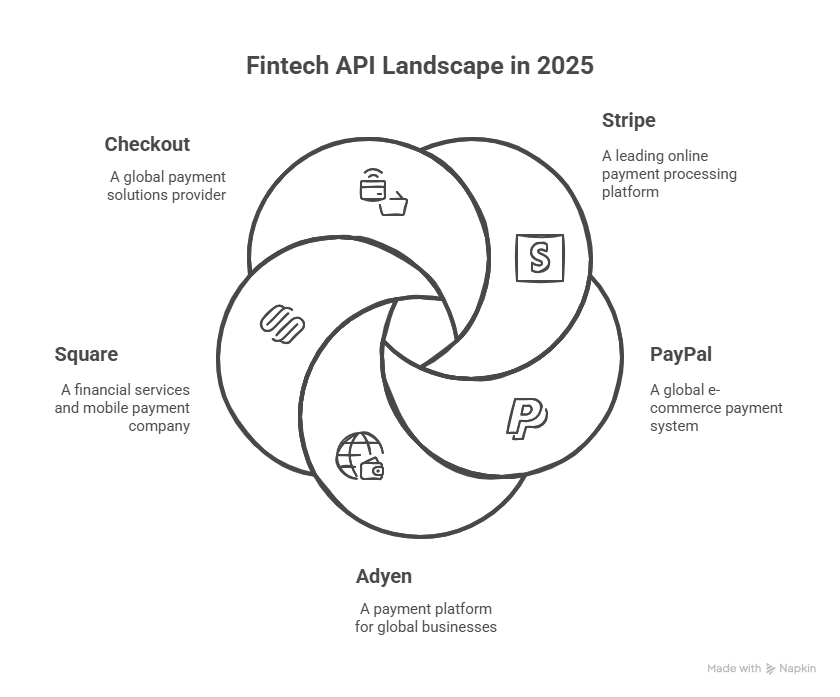

A. Payment Processing APIs

Payment processing remains the cornerstone of financial services, with payment gateway APIs handling everything from simple credit card transactions to complex international settlements and buy now pay later (BNPL) options.

Top Payment Processing APIs:

API | Processing Volume | Developer Experience | Global Coverage | Fraud Protection | Key Differentiator |

|---|---|---|---|---|---|

Stripe | $800B+ annually | ★★★★★ | 50+ countries | Advanced ML | Developer experience |

PayPal | $1.2T+ annually | ★★★☆☆ | 200+ markets | Risk management | Consumer trust |

Adyen | $720B+ annually | ★★★★☆ | 90+ markets | RevenueProtect | Authorization rates |

Square | $170B+ annually | ★★★★☆ | 15+ countries | Integrated tools | SMB focus |

$230B+ annually | ★★★★☆ | 45+ markets | Transaction routing | Authorization uplift |

Stripe continues to dominate the payment processing landscape in 2025, processing over $800 billion annually across 50+ countries. Their API stands out for its exceptional developer experience, comprehensive documentation, and robust reliability (99.99% uptime in 2024). Key strengths include their unified platform for online and in-person payments, advanced fraud prevention with Radar using machine learning, support for 135+ currencies, and comprehensive subscription management capabilities.

PayPal's API suite has undergone significant modernization, making it a powerful contender in 2025. With over 400 million active users globally, PayPal offers unparalleled reach and consumer trust. Their simplified checkout experience drives higher conversion rates for e-commerce, while their advanced risk management tools and seamless cross-border commerce capabilities make them particularly strong for international businesses.

Adyen has emerged as the preferred solution for enterprise-scale operations, particularly those with global footprints. Their unified commerce approach provides consistent experiences across channels with superior authorization rates (industry-leading by 3%). Their interchange++ pricing model offers transparency but requires significant volume to maximize value.

Square continues to excel in the SMB space while making significant inroads into mid-market organizations. Their developer platform has matured considerably since 2020, offering integrated in-person and online payment processing alongside comprehensive business management tools. Their straightforward pricing at 2.6% + $0.10 per transaction makes them particularly attractive for businesses with higher average transaction values.

Checkout.com has solidified its position as a premium payment provider focused on maximizing authorization rates and providing deep insights. Their industry-leading authorization rates (up to 6% higher than competitors) and unified API across all payment methods make them attractive for businesses where maximum conversion is critical.

Implementation Considerations:

When implementing payment processing APIs, organizations should prioritize:

- Conversion optimization capabilities

- Compliance with regional regulations (particularly PSD2 in Europe)

- Chargeback and dispute management features

- Tokenization and data encryption measures

- Settlement timing and reconciliation processes

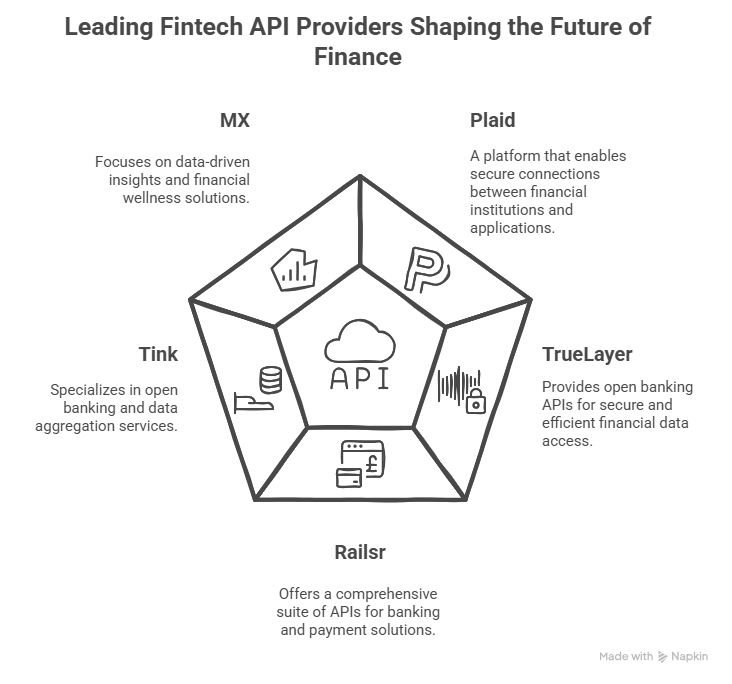

B. Banking and Open Banking APIs

The open banking revolution has fundamentally transformed how financial data is accessed and shared. In 2025, banking API solutions offer unprecedented visibility into accounts, transactions, and financial behaviors.

Leading Banking APIs:

API | Institution Coverage | Real-time Capabilities | Data Enrichment | Account Types | Regional Strength |

|---|---|---|---|---|---|

Plaid | 12,000+ institutions | ★★★★☆ | ★★★★☆ | Banking, investment, credit | North America |

TrueLayer | 3,000+ institutions | ★★★★★ | ★★★☆☆ | Banking, payment initiation | Europe |

Railsr | 50+ core integrations | ★★★★★ | ★★★☆☆ | Full banking-as-a-service (BaaS) | Global |

Tink | 3,400+ institutions | ★★★★☆ | ★★★★★ | Banking, mortgage, pension | Europe |

MX | 16,000+ connections | ★★★☆☆ | ★★★★★ | Banking, investment, lending | North America |

Plaid has maintained its position as the market leader in banking data aggregation, despite increased competition. Their network now encompasses over 12,000 financial institutions globally, providing exceptional account authentication and verification, transaction enrichment with merchant identification, and comprehensive investment account data aggregation. Plaid's pricing structure remains volume-based, typically starting at $0.25-0.50 per connected account monthly.

TrueLayer has emerged as Europe's dominant open banking API provider, capitalizing on PSD2 regulations to deliver robust connectivity across the region. Their standout features include pan-European coverage with local regulatory compliance, account information and payment initiation services, and recurring payment capabilities with enhanced user verification and authentication.

Railsr has evolved from basic banking-as-a-service (BaaS) to a comprehensive embedded finance platform, allowing companies to integrate complex financial services. They provide full banking infrastructure via API, card issuing and processing, global IBANs and accounts, and integrated credit products with comprehensive compliance support.

Tink has expanded beyond its European roots to become a global player in open banking infrastructure, offering enhanced data services beyond basic connectivity. Their account aggregation spans 18 European markets with personal finance management tools, risk insights, and sophisticated income verification capabilities.

MX differentiates itself through superior data cleansing and enrichment, transforming raw financial data into actionable insights. Their artificial intelligence-powered financial health scores, comprehensive money management tools, and advanced analytics provide sophisticated user segmentation and targeting capabilities.

Open Banking Impact:

According to the Open Banking Impact Report 2024, institutions implementing open banking APIs have seen:

- 31% increase in customer acquisition

- 27% reduction in onboarding costs

- 42% improvement in credit decision accuracy

- 63% enhancement in fraud detection capabilities

Implementation Considerations:

When selecting banking APIs, organizations should evaluate:

- Coverage of relevant financial institutions

- Data refresh frequency and reliability

- Enrichment capabilities beyond raw data

- API security and compliance certifications

- User experience during authentication flows

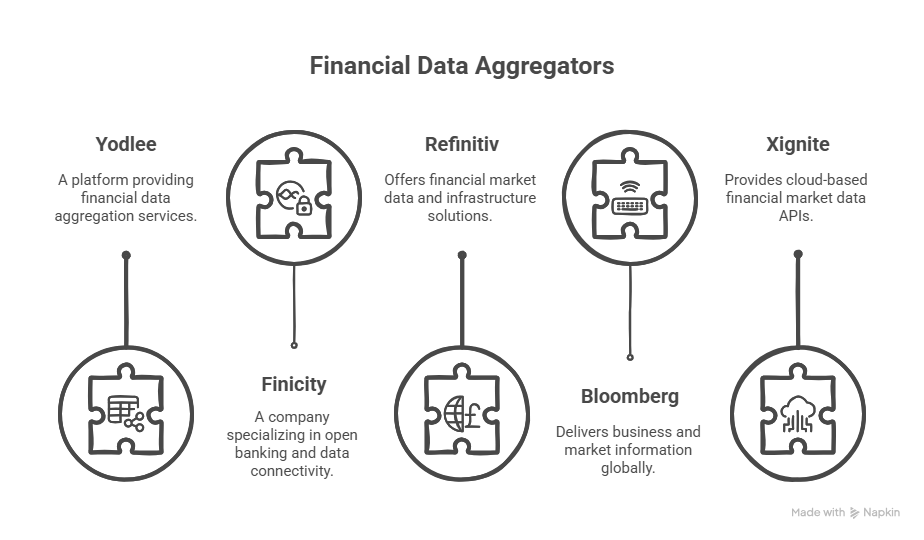

C. Financial Data and Analytics APIs

Financial data APIs provide the raw material for informed decision-making, offering access to market data, company fundamentals, alternative data sets, and sophisticated analytics through big data analytics.

API | Data Sources | Coverage | Historical Depth | Update Frequency | Key Strength |

|---|---|---|---|---|---|

Yodlee | 18,000+ | Global | 25+ years | Near real-time | Transaction enrichment |

Finicity | 10,000+ | US-focused | 10+ years | Real-time | Lending verification |

Refinitiv | 500+ exchanges | Global markets | 50+ years | Milliseconds | Institutional quality |

Bloomberg | 330+ exchanges | Global markets | 80+ years | Real-time | Reference data |

Xignite | 250+ sources | Global markets | 25+ years | Milliseconds | Cloud computing architecture |

Yodlee has leveraged its long history in financial data aggregation to build one of the most comprehensive financial data API platforms available. With data from over 18,000 global sources and 25+ years of historical transaction data, they offer advanced data enrichment, categorization, and predictive analytics with extensive compliance certifications.

Finicity (acquired by Mastercard) has expanded its data offerings while maintaining its reputation for accuracy and reliability. Their real-time account verification, cash flow analytics, and specialized mortgage verification reports make them particularly strong for lending use cases.

Refinitiv (LSEG Data & Analytics) provides institutional-grade financial data and analytics, serving the needs of sophisticated financial operations. Their real-time market data spans all asset classes with comprehensive company fundamentals, ESG scores, and economic indicators.

Bloomberg API provides programmatic access to the industry-standard Bloomberg Terminal data, offering unparalleled depth for investment applications. Their comprehensive market data covers global markets with reference data for 50+ million securities and sophisticated analytics engines.

Xignite specializes in cloud computing-delivered financial market data, offering flexible delivery models for diverse use cases. Their cloud-native architecture provides 99.99% uptime with comprehensive market data coverage at cost-effective pricing models suitable for both startups and enterprises.

Data Security Considerations:

Financial data APIs require exceptional attention to security and privacy. Key considerations include:

- Data residency and sovereignty requirements

- End-user consent management

- Data encryption standards (minimum AES-256)

- API authentication and access controls

- Audit trails and compliance reporting

According to the Financial Data Security Council, organizations implementing comprehensive API security measures experienced 76% fewer data incidents than those with baseline protections.

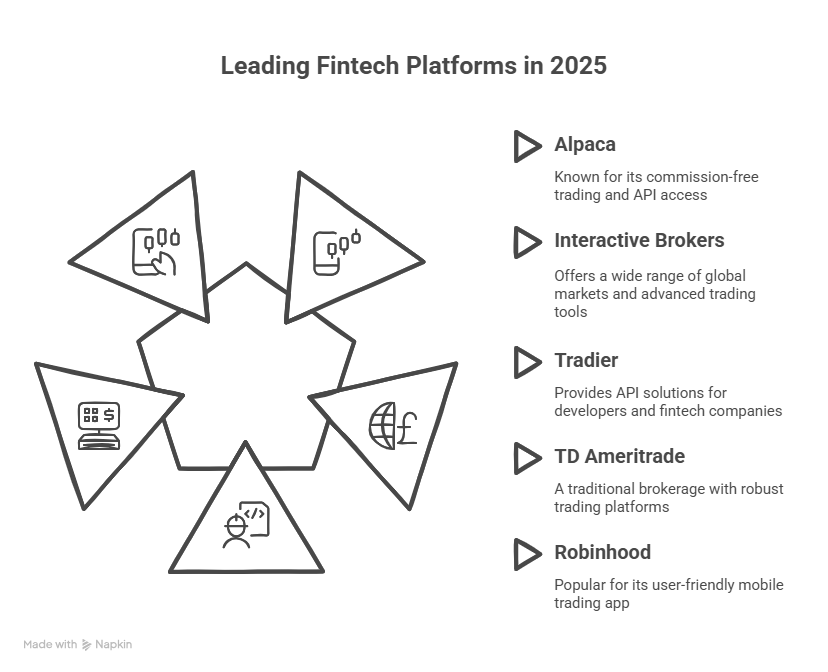

D. Investment APIs

Investment APIs have democratized access to markets, enabling organizations to build sophisticated trading capabilities without massive infrastructure investments. These APIs are particularly important for wealth management and robo-advisors.

API | Commission Structure | Asset Classes | Market Coverage | Advanced Orders | Execution Speed (ms) | Price Improvement |

|---|---|---|---|---|---|---|

Alpaca | Commission-free | Stocks, ETFs | US markets | Yes | 172 | $0.0015/share |

Interactive Brokers | Volume-tiered | Multi-asset | 150+ markets | Extensive | 94 | $0.0047/share |

Tradier | $0.35/contract | Stocks, options | US markets | Yes | 156 | $0.0021/share |

TD Ameritrade | $0 stocks/ETFs | Multi-asset | US markets | Yes | 143 | $0.0018/share |

Robinhood | Commission-free | Stocks, crypto | US markets | Limited | 182 | $0.0009/share |

Alpaca has emerged as the developer-focused platform of choice for building investment applications, offering commission-free trading via API. Their key strengths include commission-free stock trading, real-time and historical market data, fractional shares support, and comprehensive paper trading environments for testing.

Interactive Brokers provides institutional-grade API access with global market coverage and sophisticated order types. Their access to 150+ global markets with multi-asset class support, advanced order types, and comprehensive historical data make them ideal for sophisticated trading applications.

Tradier offers flexible brokerage APIs with transparent pricing, catering to both individual developers and enterprise platforms. Their equity and options trading, streaming market data, and white-label capabilities make them attractive for platform builders.

TD Ameritrade (now part of Charles Schwab) maintains a powerful API platform for retail trading applications. Their stocks, ETFs, options, and futures trading capabilities with streaming market data and comprehensive option chain analytics continue to attract developers.

Robinhood's impact on the industry warrants inclusion, despite limited official API support. Third-party solutions enable integration with their commission-free trading model, fractional shares, and cryptocurrency trading capabilities.

Implementation Considerations:

When implementing investment APIs, organizations should evaluate:

- Regulatory compliance requirements in target markets

- Account opening and KYC/AML integration

- Order execution quality and routing practices

- Real-time data requirements and costs

- Risk management and position limitation tools

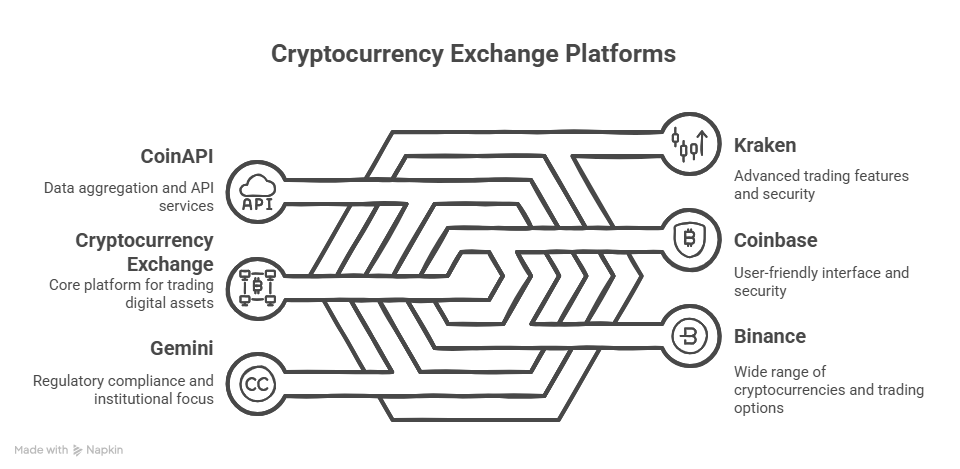

E. Blockchain and Cryptocurrency APIs

Blockchain APIs for finance enable organizations to incorporate digital wallets and cryptocurrency into their financial applications without managing complex infrastructure. These APIs are essential for DeFi (Decentralized Finance) integration.

Coinbase has established itself as the enterprise-grade cryptocurrency platform, with comprehensive API capabilities and institutional focus. Supporting 150+ cryptocurrencies with advanced security features (95% cold storage) and fiat on/off ramps in 100+ countries, they offer institutional-grade custody solutions with comprehensive compliance tools.

Binance offers the most comprehensive trading API in terms of supported assets and global liquidity. Their support for 350+ cryptocurrencies with the highest global trading volumes makes them appealing for applications requiring maximum asset coverage and liquidity.

CoinAPI specializes in cryptocurrency market data, offering standardized access across hundreds of exchanges. Their unified data from 390+ exchanges with historical data dating to 2010 provides standardized symbology and comprehensive market coverage.

Gemini focuses on regulatory compliance and security, making it suitable for regulated financial institutions entering the crypto space. Their SOC certifications, sophisticated custody solutions, and comprehensive insurance coverage reduce implementation risk for regulated entities.

Kraken provides a balance of extensive asset support, security, and advanced trading features. Supporting 120+ cryptocurrencies with advanced order types, proof of reserves auditing, and institutional-grade custody solutions, they maintain strong regulatory compliance globally.

Security and Regulatory Challenges:

Cryptocurrency API integration presents unique security challenges. According to Chainalysis State of Crypto Security 2024, organizations should implement:

- Multi-signature wallet architectures

- Hardware security modules for key storage

- Comprehensive address whitelisting

- Transaction anomaly detection using artificial intelligence

- Regular security audits and penetration testing

Regulatory frameworks continue to evolve rapidly, with significant variations by jurisdiction. The Financial Action Task Force recommends specific compliance measures for virtual asset service providers that should be incorporated into any implementation strategy.

F. Identity Verification and KYC APIs

Identity verification APIs have become a critical component of financial services, with specialized APIs streamlining KYC processes while enhancing security and compliance. These are essential for regulatory compliance in financial services.

API | Document Coverage | Biometric Verification | Business Verification | Global Coverage | Processing Time |

|---|---|---|---|---|---|

Onfido | 4,500+ document types | Advanced liveness | Limited | 195+ countries | 15 seconds avg. |

Jumio | 3,500+ document types | Video verification | Comprehensive | 200+ countries | 30 seconds avg. |

Veriff | 10,000+ document types | NFC-enhanced | Yes | 190+ countries | 6 seconds avg. |

Trulioo | 5,000+ document types | Basic | Comprehensive | 195+ countries | 60 seconds avg. |

Persona | Customizable | Liveness detection | Yes | 200+ countries | 12 seconds avg. |

Onfido has emerged as the leader in artificial intelligence-powered identity verification, offering document and biometric solutions with exceptional accuracy. Their document verification across 4,500+ document types with facial biometric verification, seamless omnichannel integration, and customizable workflow management provides flexibility while maintaining global compliance.

Jumio provides end-to-end identity verification with advanced orchestration capabilities for complex KYC workflows. Their AI-powered verification with video authentication, continuous monitoring capabilities, and advanced fraud detection systems make them attractive for organizations with sophisticated compliance requirements.

Veriff differentiates through its decision engine accuracy and exceptional fraud prevention capabilities. Their verification across 10,000+ document types with NFC scanning for chip-based documents and sophisticated spoofing detection delivers industry-leading security.

Trulioo specializes in global identity verification with exceptional coverage in emerging markets and challenging jurisdictions. Their coverage across 195+ countries with business verification capabilities, AML watchlist screening, and ultimate beneficial owner verification makes them particularly strong for global organizations.

Persona offers a highly flexible verification platform with dynamic workflow capabilities and exceptional developer experience. Their no-code workflow configuration, dynamic document selection, and comprehensive case management provide maximum implementation flexibility.

Regulatory Compliance Features:

Identity verification APIs must address increasingly complex regulatory requirements. Key capabilities include:

- Sanctions and PEP screening

- Risk-based approach implementation

- Ongoing monitoring capabilities

- Auditability and record retention

- Cross-border compliance management

According to KYC Benchmark Report 2024, organizations implementing API-driven verification reduced compliance costs by 47% while improving accuracy by 31%.

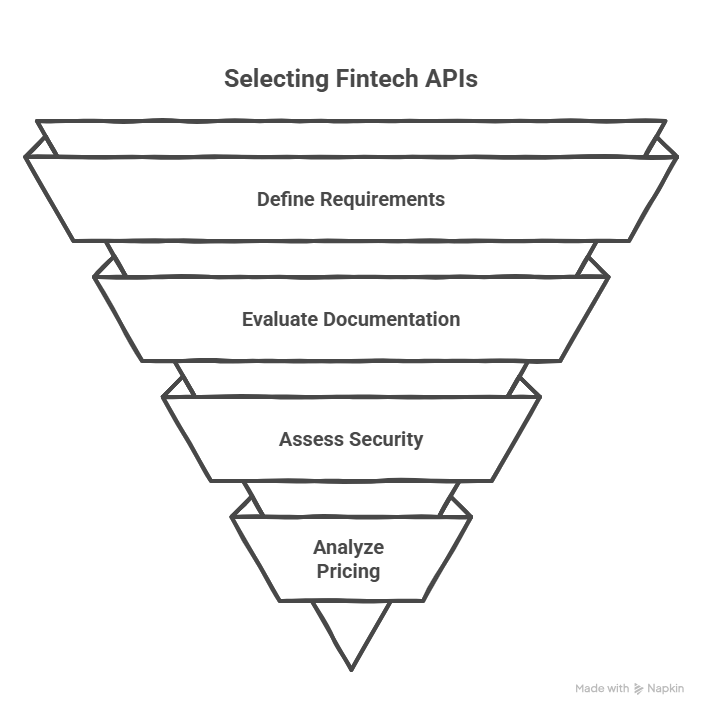

How to Select the Right Fintech APIs for Your Business

Selecting appropriate fintech APIs requires a structured approach to ensure alignment with business objectives and technical requirements.

Defining Your Requirements and Use Cases

Begin by clearly articulating what functionality you need and how it serves your broader business goals. Document specific use cases with acceptance criteria and performance expectations. This foundation enables effective evaluation of potential providers against concrete requirements rather than marketing claims.

Evaluating API Documentation and Developer Support

The quality of fintech API documentation often predicts implementation success. According to a 2024 Developer Experience Survey, 76% of failed API integrations resulted from inadequate documentation or support.

Look for:

- Interactive API explorers and reference documentation

- Comprehensive code samples in relevant languages

- Detailed error code documentation

- Active developer forums or communities

- Responsive support channels with reasonable SLAs

Assessing Security and Compliance Features

Financial APIs demand exceptional security practices. Evaluate potential providers against these criteria:

- SOC 2 Type II compliance (minimum)

- PCI DSS compliance for payment handling

- Implementation of OAuth 2.0 with PKCE

- Robust data encryption practices (TLS 1.3+)

- Regular penetration testing and vulnerability assessments

- Comprehensive audit logging capabilities

Analyzing Pricing Models and Cost Structure

Fintech API pricing structures vary widely and can significantly impact total cost of ownership. Consider:

- Transaction-based vs. subscription pricing

- Volume discounts and tiering structures

- Hidden costs (support, additional features, overages)

- Minimum commitments and contract terms

- Geographic or feature-based pricing variations

Understanding the full cost implications beyond the headline pricing is essential for accurate budgeting and ROI analysis.

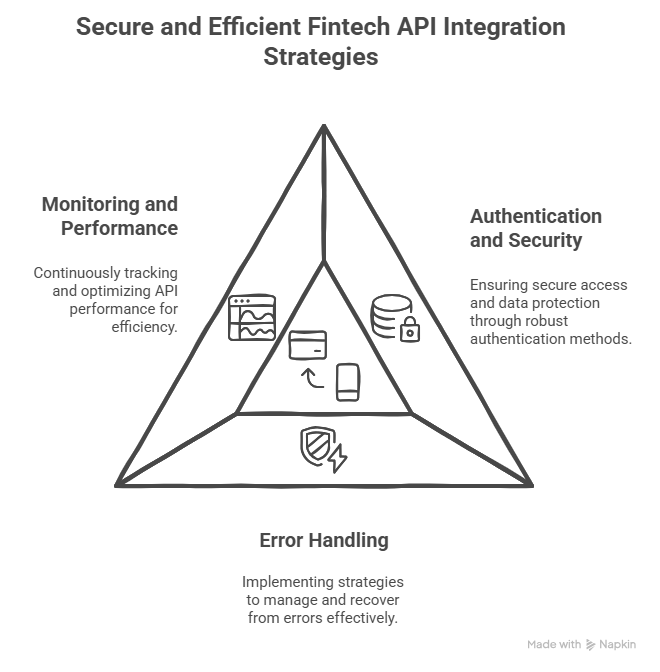

Integration Best Practices for Fintech APIs

Successful fintech API integration requires attention to security, reliability, and performance considerations throughout the development lifecycle.

Authentication and Security Best Practices

Financial API security demands multiple layers of protection:

- Implement proper API key management with regular rotation

- Use OAuth 2.0 with PKCE for user authorization flows

- Implement JSON Web Tokens (JWT) for secure communication

- Store sensitive credentials in secure vaults (e.g., HashiCorp Vault, AWS Secrets Manager)

- Implement IP whitelisting for server-to-server communications

- Use mutual TLS for high-security integrations

- Follow the principle of least privilege for all API credentials

- Consider implementing two-factor authentication (2FA) for sensitive operations

According to the OWASP API Security Project, broken authentication remains the most common vulnerability in financial API implementations.

Error Handling and Fallback Strategies

Robust error handling improves reliability and user experience:

- Implement comprehensive error classification and handling

- Develop intelligent retry strategies with exponential backoff

- Create graceful degradation paths for critical functions

- Maintain fallback providers for essential services

- Implement circuit breakers to prevent cascading failures

- Provide meaningful error messages to end-users without exposing sensitive details

Monitoring and Performance Optimization

Effective operational visibility requires comprehensive monitoring:

- Track API rate limits and usage patterns

- Implement distributed tracing for complex request flows

- Log all API interactions with appropriate detail levels

- Create alerting based on error rates and response times

- Monitor daily/monthly usage against quotas and budgets

- Implement anomaly detection for unusual API behavior using machine learning

The FinOps API Usage Report 2024 found that organizations with mature API monitoring reduced their API costs by an average of 23% through optimized usage patterns.

Case Studies: Successful Fintech API Implementations

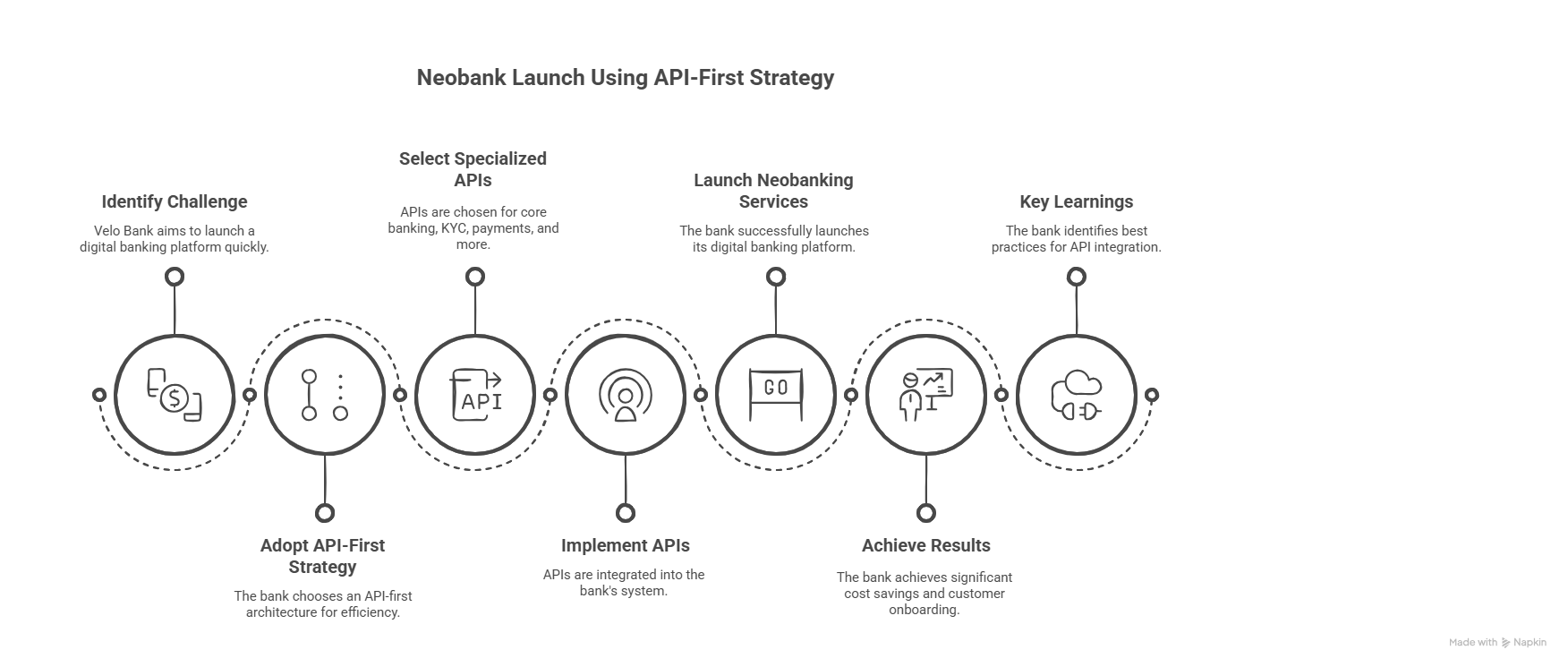

Case Study 1: Neobank Launch Using API-First Strategy

Company: Velo Bank (pseudonym)

Challenge: Launch a full-service digital banking platform within 6 months with limited development resources

Solution: API-first architecture using banking-as-a-service and specialized providers

Challenge: Launch a full-service digital banking platform within 6 months with limited development resources

Solution: API-first architecture using banking-as-a-service and specialized providers

Velo Bank adopted a composable architecture, selecting specialized APIs for each core function:

- Core banking: Railsr for account infrastructure

- KYC/AML: Onfido for identity verification

- Payments: Stripe for card processing and transfers

- Data enrichment: MX for transaction categorization

- Customer engagement: Twilio for communication

Results:

- Launched fully compliant neobanking services in 4.5 months (vs. industry average of 18 months)

- Reduced development costs by 68% compared to building in-house

- Achieved 99.98% system reliability from day one

- Onboarded 50,000 customers in first quarter post-launch

Maintained lean engineering team of just 8 developers

Key Learnings:

- Prioritize APIs with robust sandbox environments for faster integration

- Establish a clear API governance framework from the beginning

- Implement comprehensive monitoring across all API integrations

- Create fallback options for critical customer journeys

- Maintain strong relationships with API providers for priority support

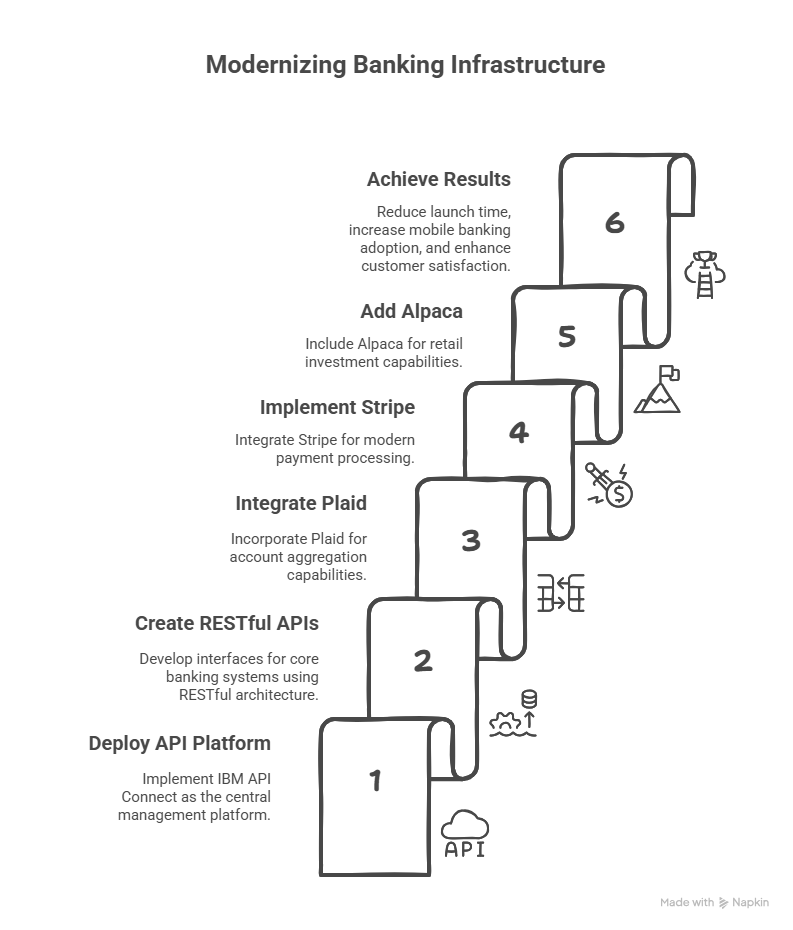

Case Study 2: Traditional Bank's Digital Transformation with APIs

Company: Regional Trust Bank (pseudonym)

Challenge: Modernize legacy infrastructure to compete with fintech challengers

Solution: API gateway strategy to expose legacy systems securely

Challenge: Modernize legacy infrastructure to compete with fintech challengers

Solution: API gateway strategy to expose legacy systems securely

RTB implemented a strategic API transformation:

- Deployed IBM API Connect as central management platform

- Created RESTful APIs interfaces for core banking systems

- Integrated Plaid for account aggregation capabilities

- Implemented Stripe for modern payment processing

- Added Alpaca for retail investment capabilities

Results:

- Reduced new product launch time from 18 months to 8 weeks

- Increased mobile banking adoption by 137%

- Decreased development costs by 41%

- Enhanced customer satisfaction scores by 28 points

Established new revenue streams through Banking-as-a-Service (BaaS)

Key Learnings:

- Start with high-impact customer journeys for quick wins

- Implement robust API security practices from day one

- Create a center of excellence for API development

- Invest in developer education and documentation

- Establish clear performance metrics for API success

Regulatory Considerations for Fintech API Integration

Financial API implementations must navigate complex regulatory environments that vary significantly by region.

Regulatory Framework | Region | Key Requirements | API Impact |

|---|---|---|---|

PSD2 | Europe | Strong customer authentication, third-party access | Authentication flows, consent management |

GDPR | Europe | Data processing, storage, consumer rights | Data minimization, retention policies |

Open Banking | UK/Australia | Standardized API specifications | Technical standards compliance |

FedRAMP | US | Security standards for cloud services | Infrastructure requirements |

CCPA/CPRA | California | Consumer rights regarding data | Consent and data management |

NYDFS | New York | Cybersecurity requirements | Security controls, reporting |

According to Deloitte's Regulatory Outlook 2024, organizations face an average of 220 regulatory updates daily across global financial markets. This regulatory complexity makes API-driven approaches particularly valuable, as they can encapsulate compliance requirements and adapt quickly to regulatory changes.

Compliance Challenges and Solutions

API-driven financial services face specific compliance challenges:

- Consent Management: Implementing granular, revocable consent for data access

- Cross-Border Data Transfers: Navigating restrictions on personal data movement

- Audit Trails: Maintaining comprehensive logs for regulatory examination

- Service Provider Oversight: Ensuring third-party API providers meet compliance standards

- Regulatory Reporting: Generating accurate, timely reports across jurisdictions

Solutions increasingly incorporate "compliance-as-code" approaches, with automated policy enforcement through API gateways, programmatic consent management, and integrated regulatory reporting capabilities.

Emerging Trends in Fintech APIs for 2025 and Beyond

AI and Machine Learning Enhanced Financial APIs

Artificial intelligence is transforming financial APIs from passive data conduits to active decision support systems. According to FinTech AI Adoption Survey 2024, 73% of financial institutions now leverage AI-enhanced APIs for risk assessment, fraud detection, and personalization.

Key developments include:

- Predictive fraud detection with 97%+ accuracy

- Real-time credit decisioning in under 3 seconds

- Hyper-personalized product recommendations

- Automated document processing and data extraction

- Customer behavior modeling and anomaly detection

Embedded Finance and Banking-as-a-Service (BaaS)

The embedded finance revolution continues to accelerate, with non-financial brands integrating financial services directly into their customer journeys. McKinsey's Embedded Finance Report projects the market will reach $7 trillion by 2026, representing 10% of all US financial transactions.

Leading innovations include:

- Single API access to comprehensive banking infrastructure

- Embedded insurance at point of purchase

- Integrated investment capabilities within lifestyle apps

- Buy now pay later (BNPL) seamlessly integrated into e-commerce

- Identity verification as a service across platforms

Real-time Payment and Cross-border Optimization

Instant payment capabilities are becoming table stakes rather than differentiators. The Federal Reserve's FedNow service and similar global initiatives have accelerated the shift toward real-time settlement.

Emerging capabilities include:

- API-accessible real-time payment rails

- Cross-border instant settlements

- Request-to-pay functionality

- Variable settlement timing options

- Programmable payment splitting and routing

Decentralized Finance (DeFi) and Sustainable Finance APIs

DeFi (Decentralized Finance) protocols have matured significantly, with APIs now providing access to sophisticated financial primitives built on blockchain infrastructure. Simultaneously, ESG considerations have moved from niche to mainstream, with specialized APIs providing critical data and analytics.

Notable developments include:

- Unified APIs accessing multiple DeFi protocols

- ESG scoring and analytics for investment decisions

- Carbon footprint calculation for financial products

- Impact measurement and reporting frameworks

- Regulatory compliance automation for ESG disclosures

Your Next Big Step in Fintech API

If you are looking to integrate fintech APIs into your application

Conclusion

The fintech API landscape offers unprecedented opportunities for innovation and competitive advantage. Organizations that strategically implement these powerful tools are seeing dramatic improvements in development speed, customer experience, and operational efficiency.

The future belongs to organizations that strategically implement fintech APIs—defining clear objectives, selecting the right partners, and optimizing continuously. As AI, embedded finance, and decentralized technologies mature, those who master API integration will gain significant competitive advantages through operational efficiency and accelerated innovation in an increasingly digital landscape.

Our expert consultants will analyze your specific needs and provide a customized roadmap for implementing the right fintech APIs for your business.

FAQs

What is Fintech API?

A Fintech API (Application Programming Interface) allows financial apps to connect with other software or databases. It enables task like processing payment, retrieving banking information, or checking customer identities securely and efficiently.

How do APIs improve customer experience in finance apps?

APIs allow finance apps to offer real-time data, such as current balance and transaction history, which helps users stay updated; APIs also support smooth navigation and personalization features, making the app more user-friendly.

Are APIs secure for financial applications?

Yes, most fintech APIs follow strict security standards and compliance requirements, like encryption and multi-factor authentication, to protect sensitive information and prevent unauthorized access.

Why are APIs important for finance companies?

APIs help finance companies automate tasks, process transactions quickly, improve data analysis, and stay flexible with market demands. This helps companies operate more efficiently and deliver better services to their customers.